Do I Need More Then a Month's Worth of Paystubs for an Auto Loan?

Are you looking to buy a car and wondering, "Do I need more than a month's worth of pay stubs for an auto loan?"

Mar 25, 2024!What is an Earnings Statement?https://checkstubmaker.com/wp-content/uploads/2022/07/pexels-cottonbro-3943716-1-1-300x200.jpg We live in a very carefully doc...

We live in a very carefully documented society, and few things are as closely measured and cataloged as finances. From tracking revenue and expenditures for measuring profitability, to identifying financial trends and potential business opportunities, to ensuring that everything is up to date and in order for tax season, most modern organizations tend to keep a close eye on their money.

We live in a very carefully documented society, and few things are as closely measured and cataloged as finances. From tracking revenue and expenditures for measuring profitability, to identifying financial trends and potential business opportunities, to ensuring that everything is up to date and in order for tax season, most modern organizations tend to keep a close eye on their money.

And that means understanding and using an earnings statement.

Here, we take a closer look at earnings statements — what they are, why they’re important, and how to use them.

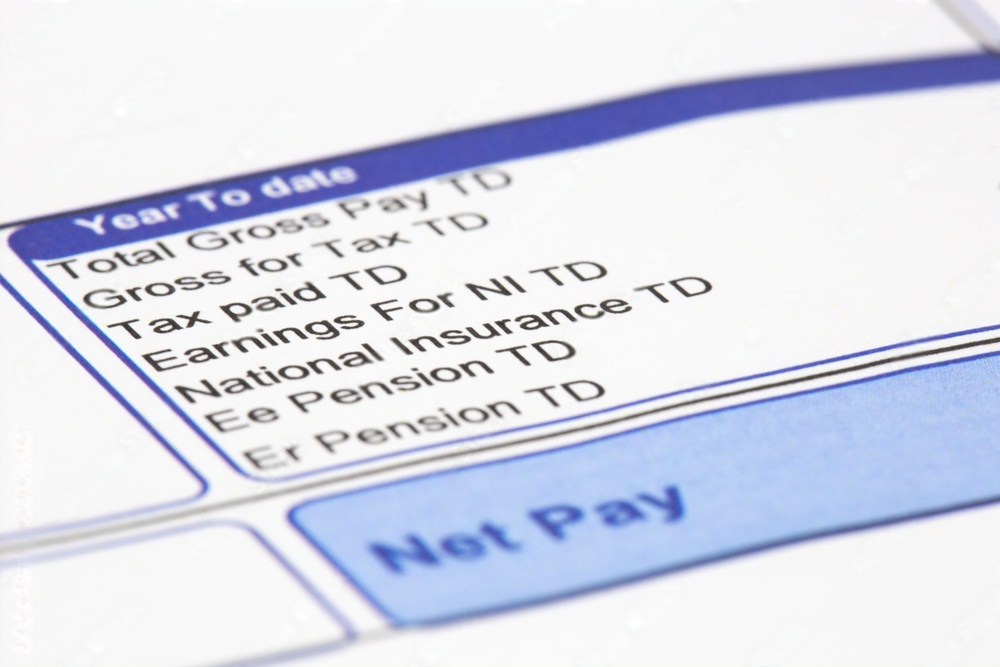

An earnings statement (also called a statement of earnings, income statement, or net income statement) is a document detailing money earned by an individual or organization during a specific time period. Performance is usually measured in terms of net profit or loss. Generally, businesses will issue an earnings statement at the end of every quarter, allowing investors to regularly analyze and track the profitability of the company. Employee earnings statements are traditionally issued alongside paychecks as pay stubs.

Whether for individual employees or entire companies, an earning statement provides important details regarding income. Individuals can see how much they’ve earned during a pay period, how much they’ve earned so far during the year and a breakdown of any deductions that might be included. Businesses rely on earning statements (along with balance sheets, cash flow statements, and statements of shareholder’s equity) to summarize their revenue and expenses across a predefined duration of time. They can then identify the company’s total profit or loss, and use that information to help evaluate current strategies.

In both cases, the earnings statement should be as clear and accessible as possible, so that users can understand at a glance the current financial situation.

It’s important to note that there is no single, universal format for an employee or organizational earnings statements. That said, nearly every earning statement will contain approximately the same information, and likely won’t be too difficult to navigate — provided you know the various terms and how they relate to one another.

In addition to the employee’s name, an individual’s earning statement will include the following components:

An earning statement for a business details business profitability for a specified time period. It usually includes the following elements:

**Time period The length of time covered in the earnings statement.

**Revenue A breakdown of all of the company’s total revenue, including operating and non-operating revenue.

**Gains Income generated by other activities, such as one-time sales of assets or equipment (other than inventory).

**Expenses A breakdown of the total expense, including all primary-activity expenses such as wages, sales commissions, utilities’ costs, and transportation expenses. This also includes secondary expenses that are not related to core business activities (such as interest paid on a loan).

**Losses Any expenses accrued from lawsuits, one-time or unusual costs, or loss-making sales.

**Net income A final tally of the profitability of the business for the time period. Net income is calculated by adding together all revenue and gains, and then subtracting the total amount of expenses and losses. It can be represented like this:

Net income = (revenue + gains) - (expenses + losses)

Earning statements are essential to detailing and documenting income. As such, businesses and individuals should closely monitor their statements of earnings for any errors or discrepancies. Miscalculations and other issues can have far-reaching effects and should be brought to accounting departments as quickly as possible.

Want to ensure that your earning statements are always accurate? Learn more, and see what Check Stub Maker can do for you!

Are you looking to buy a car and wondering, "Do I need more than a month's worth of pay stubs for an auto loan?"

Mar 25, 2024

Wondering ‘What counts as a pay stub'? A pay stub is more than just numbers; it's a vital record showcasing your earnings and deductions.

Jul 02, 2024

Need help accessing your final pay stub from your old company and wondering, "How I got my last pay stub if employer goes out of business?"

Apr 24, 2024