Non Negotiable Pay Stub

Welcome to our informative Check Stub Maker guide on non-negotiable pay stubs!

Jun 06, 2024Have you ever wondered, "Can a bank locate a lost deposited check using the check stub?" It's a common concern, and fortunately, the answer is rooted in a bank asking for paystub and how they meticulously track each transaction.

Have you ever wondered, "Can a bank locate a lost deposited check using the check stub?" It's a common concern, and fortunately, the answer is rooted in a bank asking for paystub and how they meticulously track each transaction. How important is your pay stub in this context? Through our practical knowledge, when a deposited check goes missing, banks can often trace it through transaction histories and the details provided on your pay stubs, making them critical to the process. At Check Stub Maker, we understand the intricacies of payroll practices and provide tools like our pay stub generator to ensure you have all the necessary paperwork on hand when dealing with these financial institutions. In this article, we'll dive deep into how banks handle lost checks and the role your pay stub plays in retrieving these missing payments. What this article covers:

Banks maintain comprehensive records of cashier's checks. When you purchase a cashier's check, the bank takes the money from your account and then issues the amount of the check from its own funds, guaranteeing the payment followed by a detailed record of the transaction. If a cashier's check is reported as lost or stolen, banks have protocols to investigate and potentially replace the check. However, this may require a series of additional steps to protect the bank from potential fraud. At Check Stub Maker, we emphasize the importance of keeping your own records as well. An analysis of this product revealed that our pay stub creator helps ensure that you have all necessary documentation for transactions involving checks and payments. This provides an extra layer of security and peace of mind when it comes to managing your financial affairs.

As per our expertise, there are a few ways of handling a lost cashier's check:

At Check Stub Maker, we recommend keeping personal, detailed records of all your financial transactions, including cashier's checks. Maintaining good documentation in this regard can streamline reporting and resolving issues with lost checks.

If you lose a cashier's check, our findings show that you should notify the issuing bank immediately. From there, you'll be required to complete a declaration of loss and may need to secure an indemnity bond. This bond protects the bank in case the check is fraudulently cashed or found and presented by someone else. At Check Stub Maker, we understand that proper documentation can significantly facilitate this process with your bank and do our best to ensure a swift resolution.

Banks are required to keep a record of deposit slips. These slips serve as proof of the transaction, detailing the:

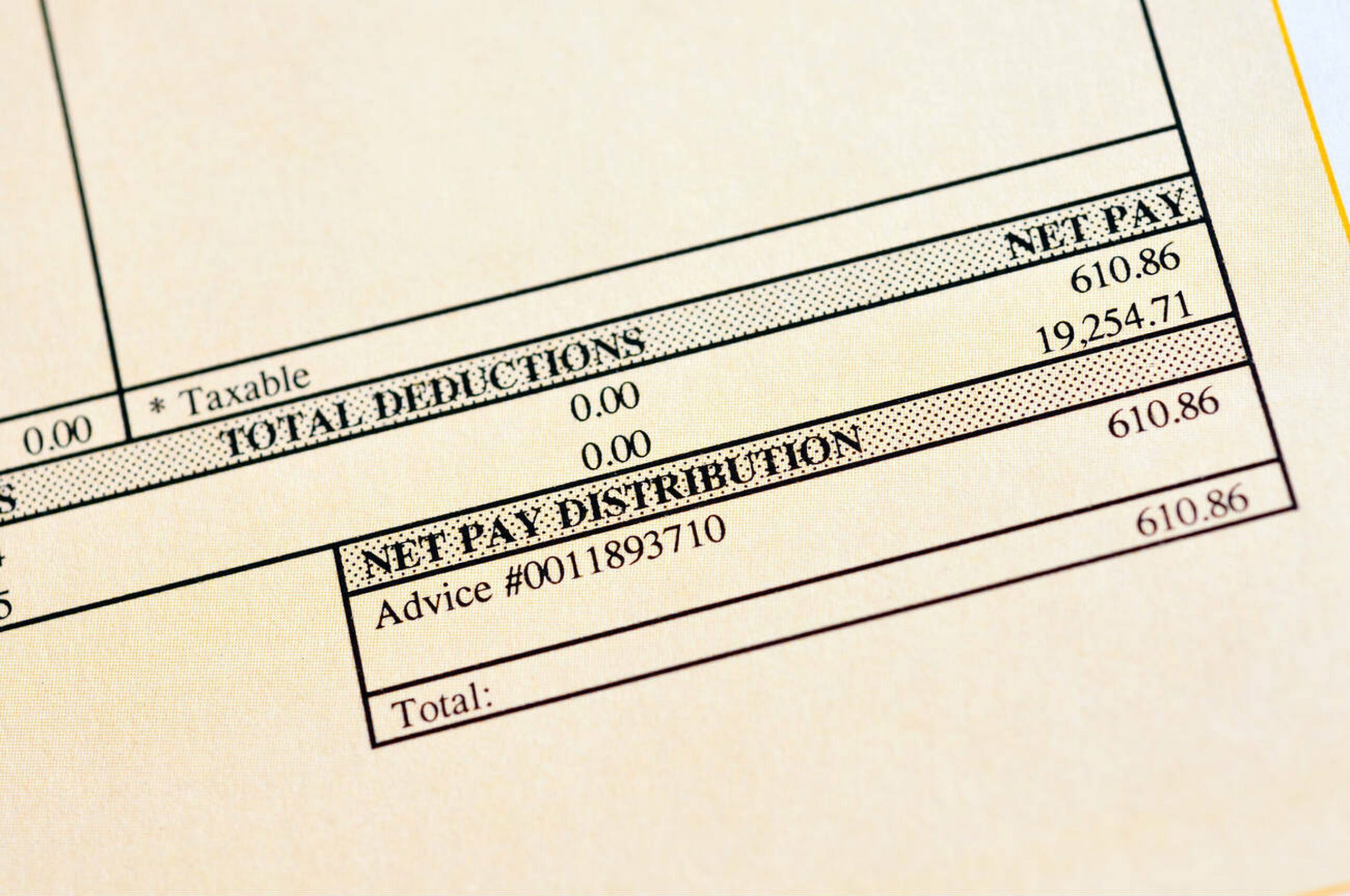

As per regulatory requirements mandated by the Bureau Of The Fiscal Service , banks must maintain these records to ensure accuracy in financial reporting and to help resolve any discrepancies that may arise with account holders' bank statements. Like direct deposits, our services at Check Stub Maker help you maintain detailed and accurate records, complementing the paperwork held by your bank. After putting it to the test, this dual record-keeping can be crucial in confirming transactions and providing peace of mind in all your financial dealings.

When an employee reports that their direct deposit hasn't been properly credited to their bank account, particularly when there's a severance pay stub but no check received , it can cause a great deal of concern and confusion. Here's how employers can efficiently handle this kind of situation.

First, ensure that there hasn't been a simple misunderstanding regarding the pay date. Sometimes, discrepancies arise because of differences in bank processing times or misunderstandings about the scheduled date for deposit. It's important to check that the funds were indeed meant to be released on the expected date. Employees should check their bank accounts again after confirming the proposed pay date, as banks can sometimes have delays in displaying the deposit on their systems. When you create pay stubs with us at Check Stub Maker, you can easily keep track of your pay dates and periods so you know when you're typically paid by your employer.

Next, review your payroll reports carefully. Our investigation demonstrated that this step is crucial to check that the direct deposit instructions were entered correctly and that there weren't any errors with the account or routing numbers. Errors can occur, and verifying this information can rule out simple mistakes that may have prevented the deposit from going through. Additionally, ensure that this was processed on time. Delays in this regard can also lead to missed or delayed deposits.

Ensure that the payment method was correctly set to ‘direct deposit' and not a different kind of banking transaction. Sometimes, issues arise because the payment was sent through a different method such as a check, especially if the direct deposit setup was a recent addition to your company protocols. Confirm with your payroll department that the direct deposit details provided by the employee—account number, bank routing number, etc.—are accurate and were processed as expected. Miscommunications or data entry errors can occur, and it's vital to verify these details first before proceeding further.

From there, you should determine if the issue is isolated to one employee or affects multiple employees. If the latter are impacted, there might be a larger issue with the payroll system or the bank itself. Check if there are any notifications from the bank regarding delays in making payments. If only one employee is affected, our research indicates that it's more likely an issue with their specific bank account or payroll details instead of a wider issue.

Once you understand how the direct deposit error occurred, you should contact your bank's Automated Clearing House (ACH) department, which handles electronic transactions, including direct deposits. You should inquire whether there were any issues with the transaction batch that included your employee's payment. Occasionally, delays can occur due to:

It's essential to clarify that the payment was sent and received by the employee's bank first and foremost. Through our trial and error, we discovered that reaching out to the bank can often quickly clarify whether the issue is a simple banking delay or a more serious transactional error.

If direct deposit issues occur frequently, it might be worthwhile to consider alternate payment options. Offering choices such as payroll cards or paper checks can be a backup for employees who encounter recurring issues. Drawing from our experience, this approach not only provides an immediate solution but also helps in cases where bank policies or technical problems delay direct deposits. We suggest keeping flexible payment methods available to accommodate various needs and ensure that all employees have reliable access to their earned wages without interruption. By ensuring that your business workflows are adaptable and responsive with a digital system like ours at Check Stub Maker, you can prevent future issues and maintain your workforce's satisfaction and financial security.

Typically, there's a waiting period of 30 to 90 days before the bank will issue a replacement for your cashier's check. Based on our observations, this waiting period is meant to ensure that the original check is not cashed elsewhere. During this time, the indemnity bond will cover any potential loss to the bank should the original check re-surface and be cashed by someone else for fraudulent purposes.

A deposit slip is a small written form used to place funds into your bank account. This slip provides the bank with the necessary information to transact and record the deposit correctly. Through our practical knowledge, it typically includes the:

Deposit slips serve as proof of payment for the depositor and vital for maintaining accurate financial records. Retaining a copy of your deposit slip can help resolve any discrepancies with bank deposits.

The time a direct deposit hits your bank account depends on several factors, including the:

Most banks update their accounts and post deposits at midnight or early in the morning on a business day, but the exact timing can vary. In some cases, our findings show that funds can appear in the recipient's account at midnight on the day the deposit is supposed to be made. Employers often send payroll files a few days in advance, ensuring that employees receive their wages on the designated payday. At Check Stub Maker, we help our users understand these mechanisms and maintain accurate records, so that managing your transactions is seamless from start to finish.

In today's deep dive, we explored whether a bank can locate a lost deposited check using your check stubs, and how the intricate processes of banks and pay stubs facilitate tracking down those occasionally elusive payments. From traditional checks to streamlined direct deposits, understanding these mechanisms is crucial for smooth financial operations when using a pay stub form of ID or for other authentication purposes. So, why not give our tools a whirl and see how easy managing payroll can be? Visit us at Check Stub Maker to learn more and start simplifying your finances with our intuitive paystub creator today! If you want to learn more, why not check out these articles below:

Welcome to our informative Check Stub Maker guide on non-negotiable pay stubs!

Jun 06, 2024

!6 Tips & Tricks on How to Attain a Higher Credit Scorehttps://checkstubmaker.com/wp-content/uploads/2022/09/6-tips-and-tricks-300x182.jpg https://checkstubm...

Jul 27, 2022

Ever glanced at your pay stub and wondered, ‘What is the EFT no. on a check stub?' Don't fret; that's just the unique number that shows money was transferred...

Aug 31, 2023